Reflections from the NZACS Convenience and Impulse Retailing Expo.

Getting together with people on the frontline of retail is the best way to see the future unfold. Last week I got that opportunity thanks to the morning symposium at the Convenience and Impulse Retailing Expo in Auckland, hosted by NZACS.

Two presentations stood out to me: Lance Dobson from Nielsen IQ New Zealand and Theo Foukkare, CEO of the Australian Association of Convenience Stores (AACS). Together, they painted a picture of an industry under real pressure but also one brimming with opportunity for those willing to move.

The common theme running through both talks? Convenience retail is no longer about proximity. What struck me most, listening to both Lance and Theo, is how clearly their insights map to the conversation we have every day with convenience retailers about frictionless commerce — a single view of customer and inventory data across every channel.

Store sales are holding, but the mix is shifting

First up, we looked at the current landscape. Lance made an encouraging point: when you strip out fuel site closures and look at like-for-like shop sales, the convenience channel is holding up reasonably well. Non-fuel convenience stores have maintained positive same store growth into Q1 2026. Fuel-attached stores were tracking fine until the fuel price spike hit in late February.

The categories driving growth tell a clear story. Those leading the way include fresh barista coffee, sports and energy drinks, chilled beverages, snack foods, confectionery and food2go. The channel is concentrating around food and beverage, especially when delivering on quality, freshness and the in-store experience.

For retailers, this means your POS, your inventory management, your loyalty program and your food service operations all need to speak to each other in real time. A coffee loyalty card must connect to your customer data, a food2go offer must be reflected in your app. Promotions that run at the forecourt also need to be available in-store.

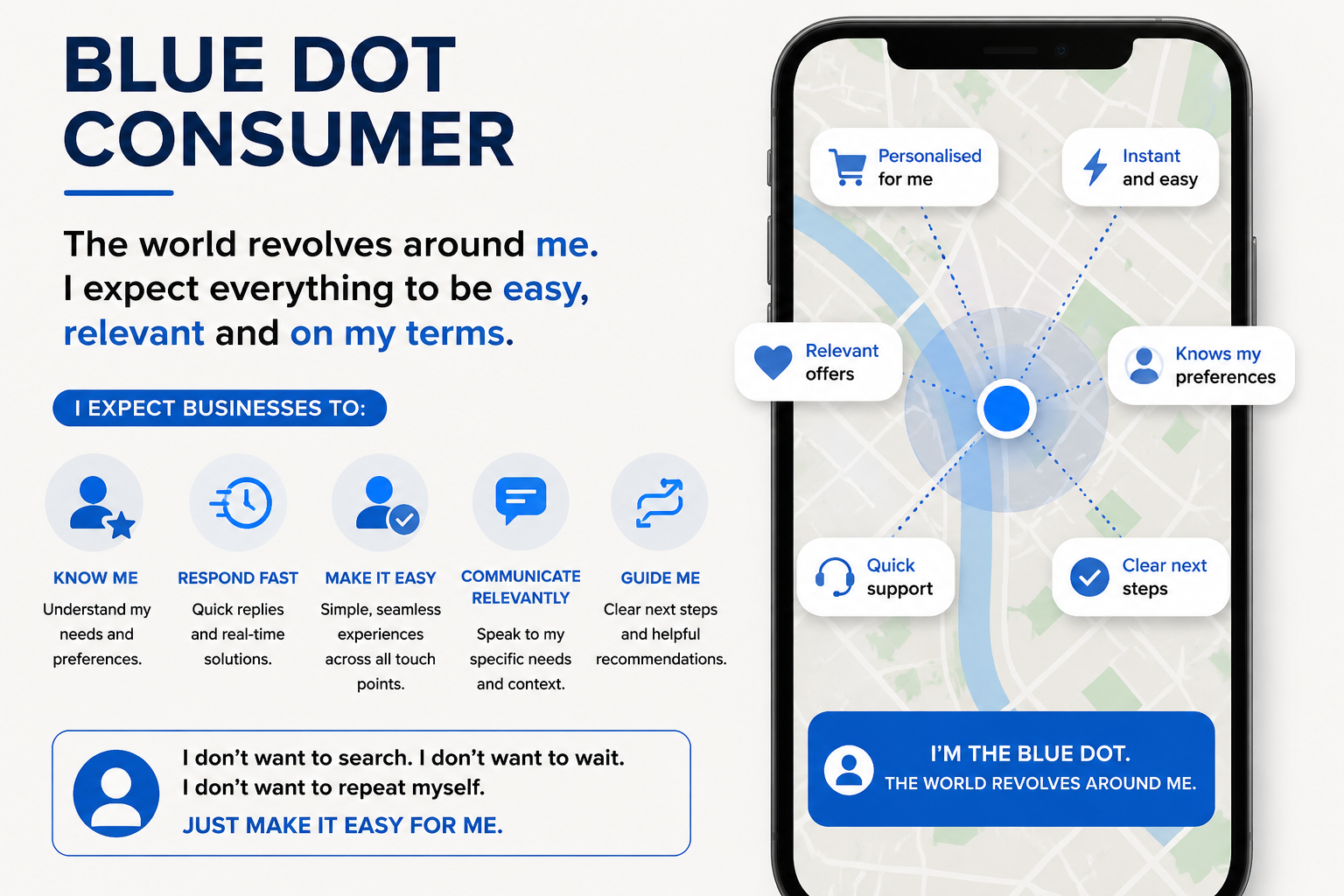

The blue dot customer and frictionless commerce

Lance introduced a concept that has stuck with me: the blue dot consumer. That little blue dot on your phone map, that’s you. Increasingly, consumers expect the world to come to them, not the other way around.

Survey responders described convenience as "everything in one place”, "close to me”, with "minimal effort”, and growing fast off a small base "deliver to me when I want it”. Lance shared that in the UK, quick commerce now accounts for nearly one pound in every ten spent on grocery retail. ANZ is behind that curve, but intention data suggests the gap will close quickly.

The implication for retailers is significant. If the customer is the fixed point and everything else has to move, then your ability to serve them across multiple channels in-store, at the pump, via app, through delivery from a single, consistent platform isn’t a nice-to-have. It’s the game.

That's what frictionless commerce looks like. It’s not multichannel or omnichannel as a buzzword. It’s a single, real-time view of the customer, the basket, the inventory and the transaction wherever that transaction happens to take place.

Lead in quick service retail

Theo was emphatic: the world’s best convenience retailers are no longer chasing fuel volume. They are chasing lifetime customer value, and the vehicle for that is quick service retail (QSR).

He pointed to Japan’s 7Eleven, where lunchtime queues form outside standalone convenience stores because customers trust the offer completely, and OTR in Australia, which is building destination stores with cafes, fresh food prep and community amenities.

Getting your food offering right is fundamental, especially as revenue from tobacco sales continues to decline. The question Theo posed to the room was sharp: “Is food a category you sell, or is it your business?”

Lance echoed this from a category data perspective: barista coffee is the number one food or drink item bought in convenience. Hot cabinet food is close behind. Quality and freshness are the decision drivers, and the retailers winning here are investing in the back-end systems that make consistency possible not just upgrading to the latest coffee machine.

“If you don’t own the customer digitally, you’re just renting them"

Both Lance and Theo emphasised the importance of loyalty. Lance noted that 60% of convenience shoppers want tangible value for their repeat visits, such as a coffee cards, linked apps. They’re less interested in traditional loyalty and more focused on personalised reward. Consumers want to feel seen and not just accumulated.

Theo took this thought further. He described retailers using technology to analyse customers as they arrive, what they’re wearing, what they’re driving, whether they’re a known customer and serving a personalised offer on-screen before they have walked through the door. The retailers building real digital ecosystems are seeing the payoff in basket size, frequency and margin.

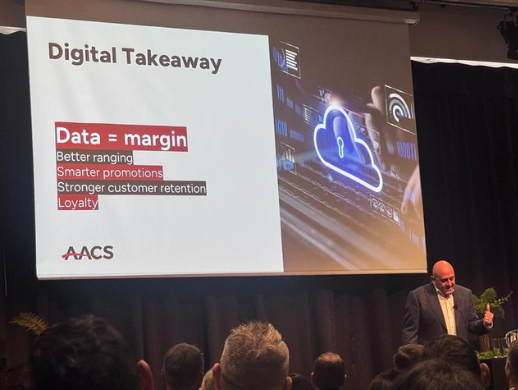

The underlying principle is data equals margin. Better data means better ranging. Better ranging means less waste, more relevance and stronger customer retention.

This is where frictionless commerce delivers its most tangible value. When your POS, your loyalty platform, your app and your inventory system all share a single view of the customer and stock position, you truly give customers what they seek. When they are siloed with different vendors, different data sets, no common customer identifier then you are left guessing.

The five forces shaping what comes next

Theo framed the future around five forces: margin pressure, transition uncertainty, changing customer expectations, digital acceleration and survival. The retailers who will thrive are those who respond across all five, not by chasing each trend but by building the operational platform to adapt quickly.

Lance’s framing was similar and focused on speed, health, innovation, flavour and technology. The winners will be those that move fast, test more, stay culturally connected and use technology to stay close to the changing rhythms of consumer life.

Both speakers landed in the same place: ”standing still is not an option”.

What frictionless commerce means for you

The convenience channel in 2026 is a food and beverage business with a fuel forecourt attached, not the other way around. Consumer missions are diversifying. The tobacco anchor is eroding. The digital expectation is rising. And the competitive set now includes QSRs, quick-commerce apps and destination food retailers.

In that environment, the retailers who win will be the ones who know their customers best, execute their offer most consistently and can adapt their ranging, pricing and promotions in near real-time.

That requires a technology foundation built for frictionless commerce with one platform that delivers a single view of customer and inventory data, tying together the forecourt, the shop floor, the kitchen, the app and everything in between — not a patchwork of systems held together with spreadsheets and goodwill.

The NZACS symposium reinforced that the shift is already happening. The question is whether your technology is positioned to move with it or whether it’s holding you back.

Interested in how frictionless commerce can support your convenience retail operation? We'd love to talk.